Snowflake

I have written about IPO’s before (A Parade of Unicorns) and that I generally avoid them. However, Snowflake, an upcoming IPO has the characteristics of a great business. I have invested a lot of time understanding the business and here are a few relevant notes on business background and potential.

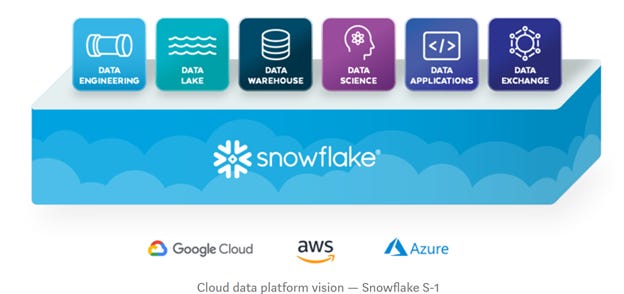

Snowflake (SNOW) is one of the most anticipated IPO’s of the year. As its names suggest, Snowflake is a born-in-the-cloud data warehouse platform. It has the potential to be a cornerstone data and analytics technology, has a track record of blistering growth, and is led by a highly respected team.

Background.

Two Oracle engineers, frustrated by the limitations of the legacy database architecture built in the late 70’s, came together (Founders Story Link) to build the data warehouse of the future. They built a system that is fast, is cheap to start, that leverages the scalability and elasticity of the cloud, and is easy to maintain. (Brief Co. Background)

What does the product do?

For most businesses large or small, data is siloed in different application databases in various departments. Therefore, it is difficult to aggregate this data and draw enterprise-level conclusions. Snowflake’s technology helps Companies extract this data from enterprise nooks and crannies, aggregate it, and store it in the cloud. Once the entire dataset is one place, it becomes much easier to deploy analytic tools to draw intelligent inferences. Disney provided a real-world use case. Disney used Snowflake to aggregate its consumer data between Disney, ESPN, Fox, and Hulu to draw conclusions to build its Disney Plus bundled offering (Link). For technical details, I suggest you read this (deep dive).

Speed, Cost, and Scalability.

The cloud infrastructure platforms (Amazon Web Services, Microsoft Azure, and Google Cloud) are the foundational blocks of the cloud. Snowflake has the potential to be a cornerstone technology for the data and analytics layer. A great feature of Snowflake is its scalability. The Company charges based on consumption, instead of a flat recurring fee, and therefore can be easily scaled up or down based on demand. Therefore, this platform can be used by companies of all different sizes – from a start-up all the way to a Fortune 50 company. For example, a million rows of data can be uploaded in a few minutes and analyzed for a few dollars. Speed, low costs, and scalability are the key differentiating characteristics of Snowflake.

Weak Supplier Power, but low gross margins.

While the reliance of the infrastructure players for compute creates a ‘frenemy’ dynamic - the infrastructure providers also have their own data warehouse offering – Snowflake has blown past competitors. Given Snowflakes’ success means more revenues for The big 3 providers, the supplier risk to the business is lower than one would believe. This can be directly seen in the lower gross margins. While most cloud-based SAAS Co’s have gross margins in the 70-80% range, SNOW’s margins are 60%. One of the few negatives.

High Switching Costs.

Porting data over from one platform to another is an arduous task, which makes data warehouse platforms sticky businesses. The Snowflake platform makes it easy to share data. An example would be a retailer, a supplier, and the logistics partner to share inventory and delivery data to improve business performance. While the network effects are weak, they nevertheless make the platform stickier and harder for customers to switch.

Business Trends

Snowflake is led by the dream team of Frank Slootman at CEO and Michael Scarpelli at CFO. This team shepherded ServiceNow (NOW) through an IPO process in 2013 and built the business into an IT services powerhouse that it is today. Revenues grew from $70 mill to $3.4 bill during their tenure. Since assuming the CEO position last year, Frank Slootman has accelerated the sales and marketing spending on pursuing large corporations. Revenue growth has accelerated to 120% in the most recent quarter and net revenue retention has averaged between 160% and 180% over the past 4 quarters. The number of large customers has also grown rapidly.

Large End Market.

The runway for Snowflake is long. The data storage end market is estimated to be $80 billion and growing rapidly. Therefore, Snowflake is less than 1% penetrated today and can grow for many more years in the future. Analytics is another large end market estimated to be $55-60 billion. So far, Snowflake has partnered with existing analytics providers. However, analytics is a natural product extension over time and an easy way to capture incremental dollars from existing customers. We should all expect an analytics offering sooner than later. In total, Snowflake is playing in, by far, the largest and the fastest-growing technology end market.

Expensive Valuation.

Based on 2021 projected revenues close to $1 billion, the accelerating growth, the large end market, and the management pedigree, the IPO is likely to be priced in the $40 billion range. A 40x EV/Sales is a massive valuation multiple, higher than any public peer today. Snowflake is clearly a unique asset, with an expensive price tag.

(These are my notes from the S1 filing and not financial advice)