Retail's Growing By Shrinking Strategy

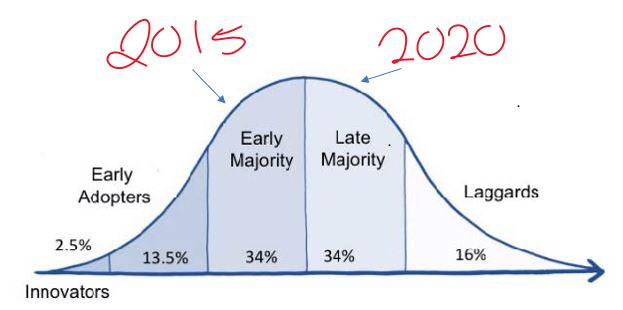

The Diffusion of Innovations is a framework created by Everett Rogers to understand how innovation spreads over time. It is a good prism to understand retail’s evolution through. Opponents of retail have been chipping away at its reign for over a decade. It took a turn for the worse in 2015 as the Amazon ecosystem tipped customer preferences dramatically towards E-commerce. In 2015, the ‘early majority’ was embracing internet retail.

Retail’s weakest links were the first to fall. Those were the undifferentiated concepts, low-tier shopping malls, and businesses without an e-commerce strategy. Retail bankruptcies rose during 2016-2017. However, U.S. tax cuts provided a one-time boost in 2018 as bankruptcies ebbed temporarily.

Covid-19 is a 1-2 punch for retail. While the duration of this pandemic is unknown, it hits hardest at the best part of retail - the social and discovery experience.

We know Covid-19 is temporary. However, the ingrained ease of ordering from the comfort of the sofa is not. Social distancing has brought the ‘late majority’ to the E-commerce party, and the scales have permanently tipped against in-store retail.

It is proven that a physical location will improve a brand’s presence in a geographic area - but the returns diminish past a few stores. Therefore, a strong E-commerce channel with fewer stores for ‘showrooming’ will provide the best future avenue for most retailers. That is an easy way for most retailers to have their cake and eat it too.

These comments from William-Sonoma (WS) are likely to be repeated by other retailers in the future -

“In the next three years, as I said, 293 stores come up for renewal. And over the next five stores, 416 come up for renewal. So, we are going to be able to make a lot of decisions based on the malls, what happens, the partnership, and the four walls that we have in each and every store. And that is, I think, a strong position to be in.”

WS operates 615 total stores and 6.5 mill sq. ft. of retail space. In 2019, more than 55% of its sales were driven by E-commerce. In 1Q of 2020, WS was able to grow sales despite closed stores. This is a clear indication that WS can grow the business and improve its financial metrics by closing stores. How many stores will the business close over the next five years?

The eagerness of the best retailers - to grow thru shrink - is bad news for the entire retail value chain.

This is what I believe.

What do you believe?

Good article. The mathematical problem facing mall softlines retail is trading Profitable store sales for Ecom sales. Trading a 50pct incremental margin for a 5pct incremental margin (if you are lucky before returns and markdowns online). As Ecom mix increase, not only do EBIT margins decline materially but EBIT dollars decline 15pct per year as we have seen for 5 consecutive years in mall apparel during this channel shift. Consumers are unwilling to pay for shipping and return rates are high for department stores and mall apparel. WSM has benefit of low return rates and charging for shipping heavy items and is less impacted by channel shift.